Feels Like 1999. But Is It?

The tape still belongs to the bulls. The margin for error is getting thinner.

Illustrative Path – Not to Scale

The market feels speculative again — not because it has to fall tomorrow, and not because investors should suddenly run for the exits. That is not the point. The point is that risk is rising at the same time confidence is rising, and that combination usually deserves more respect than it gets.

Over the last couple of months, the S&P 500 has recovered with incredible speed. The last real correction in 2025 came around the tariff scare. The decline itself happened quickly, almost violently. The recovery was not a one-day snapback, but that is the point: a meaningful drawdown was absorbed in a few weeks, as if the market had already decided every dip was temporary. The lesson keeps getting reinforced — buy the dip, do

not ask too many questions — and that lesson works until it doesn’t.

The Part That Feels Like 1999

This is the part of the cycle that reminds me of 1999. Not because today is exactly 1999. The companies are different. The policy backdrop is different. AI is not the same as the dot-com internet story. But the mood feels familiar.

You can feel it in small ways. Younger investors are trading actively. People who normally would not care about individual companies are suddenly talking about AMD, semiconductors, AI names, and how much money they have made. Someone who helps care for our children recently asked me about AMD. She does not know the business deeply. She does not need to. The stock went up, people around her are talking about it, and that becomes enough of a story. That is not a criticism of her; it is a market signal.

If you have seen The Big Short, the reference point is useful. One of the movie’s clearest insights is that speculation does not always announce itself first in a spreadsheet. Sometimes it shows up in ordinary conversation — in people becoming completely comfortable with risk they do not fully understand. The details today are different, but the rhythm is familiar. Late-cycle confidence often becomes social before it becomes

obviously dangerous.

That is how speculative phases work. The story becomes simple enough for everyone to repeat. Stocks go up. Dips are opportunities. The winners keep winning. Valuation does not matter because growth will fix it. If something falls, the market bails you out in a few weeks.

This is also the phase where the least cautious capital often looks the smartest. People who took the most risk, bought the highest-beta names, and ignored every warning can make a killing. They make disciplined investors look foolish. They make risk management feel outdated. Bullish sentiment by itself does not end a market, but when investors become more confident after a violent recovery rather than more cautious, the setup starts to look late-cycle.

The Tape Still Belongs to the Bulls

To be fair, the technical picture still belongs to the bulls. Major support has not broken. Moving averages are still supportive. Momentum still points higher. Anyone looking only at the chart can reasonably say the trend remains intact, and they would be right.

But risk does not wait for the moving averages to roll over before it starts rising. By the time every technical support breaks, the easy part of risk management is already gone. The harder part is recognizing when the market is still going up, but the quality of the move is getting worse. That is where I think we are.

Valuation Is Not a Timing Tool

Valuation is not a timing tool. Expensive markets can get more expensive. In a mania, they often do. But valuation still tells you something about forward risk and future returns.

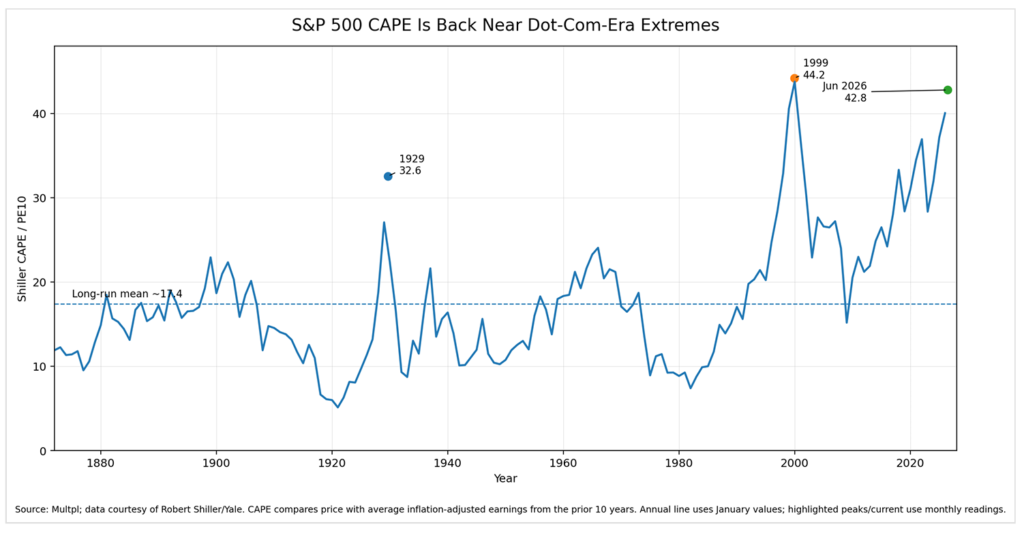

S&P 500 Shiller CAPE / PE10, 1872–2026

Source: Multpl; data courtesy of Robert Shiller/Yale. Annual line uses January values; highlighted peaks/ current use monthly readings.

When the Shiller CAPE is near the highest levels in market history, the burden of proof shifts. The market has to keep delivering. Earnings have to keep surprising. Liquidity has to keep helping. Sentiment has to stay friendly. That is a lot to ask when everyone is already leaning the same way.

This can still stretch further. A correction from here may not end the speculative phase. It may reset sentiment just enough to fuel another leg higher. If the AI IPO window opens and large private AI companies come to public markets, investors may get a fresh story, fresh supply, and a fresh excuse to push valuation further. So I am not saying this has to be the top. I am saying the risk-reward is getting worse.

The Risk-Reward Has Changed

This is not a call to sell everything. It is not a call to short the S&P 500. It is not a claim that the top has to be today, this week, or even this month. Markets can stay wild longer than disciplined people expect. In a true blow-off, price can travel much further than valuation alone would justify.

We saw a version of this in gold and silver earlier this year. The move kept going. The story kept improving. More people became convinced that the only mistake was not owning enough. Then the market stopped rewarding that thinking. No bell rang. It just stopped making new highs.

Equities may be entering a similar emotional zone now. The market can still go up another 5%, 10%, or even more. The risk is that investors treat that final stretch as proof that risk has disappeared, when it may simply be the last part of the move.

What Would Change My Mind

I would change my mind if the market broadened in a durable way. I would want to see strength move beyond the same AI, semiconductor, momentum, and high-beta names. I would want to see valuations cool without major price damage. I would want to see investors become more cautious after a big rally, not more euphoric. I would want to see a market that can rise without needing speculative heat to carry it.

Until then, I think this is a very high-risk market.

Bottom Line

The trend still favors the bulls, but the mood is starting to look too easy, too confident, and too forgiving. That is not when I want to become more aggressive. That is when I want to manage exposure, respect gains, and remember that markets usually feel safest somewhere near the point where risk is actually rising.

This may not be 1999, but it rhymes enough to pay attention.

Opinion for educational purposes only; not investment advice.